SP500 LDN TRADING UPDATE 18/3/26

SP500 LDN TRADING UPDATE 18/3/26

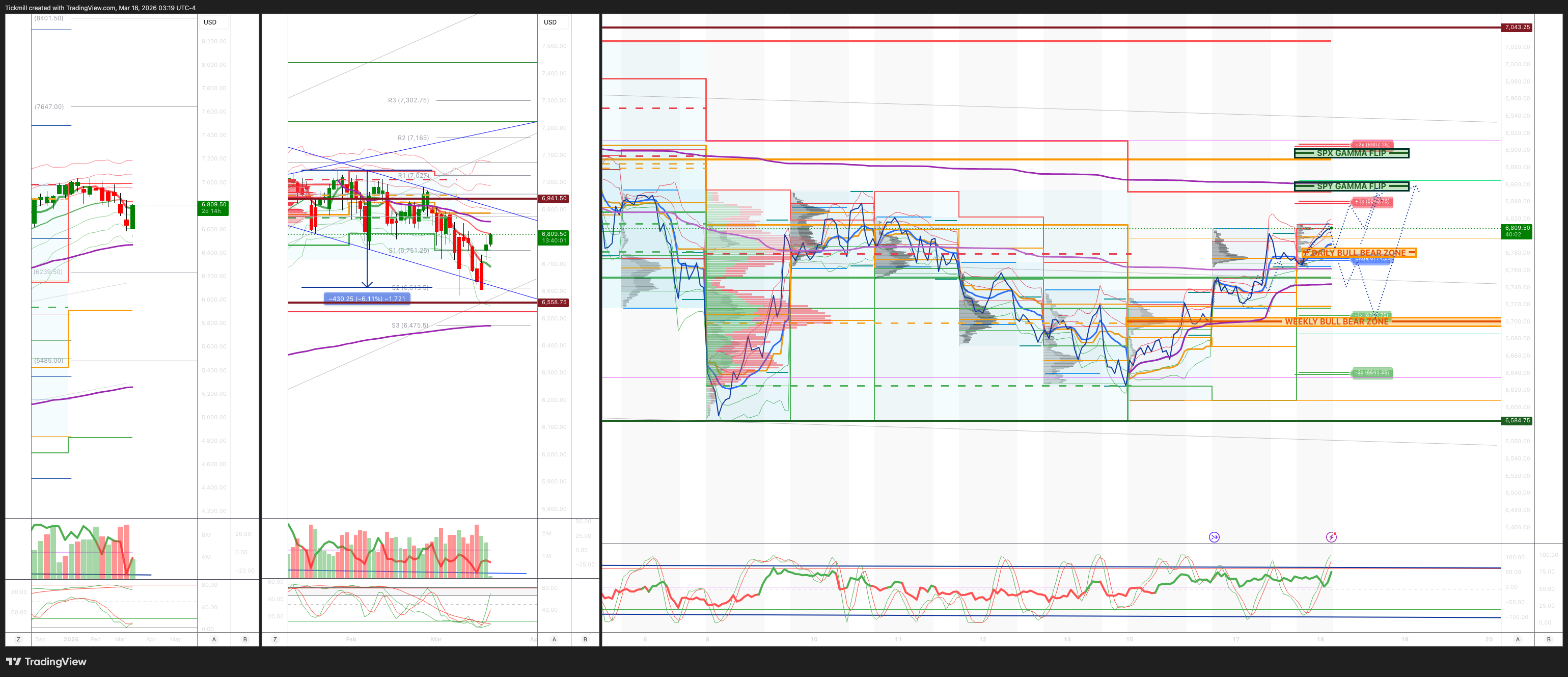

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6700/10

WEEKLY RANGE RES 6825 SUP 6426

Weekly Straddle Range: 199 -point straddle implies a weekly range of [6426, 6824]; monitor 1.5x and 2x moves for key reactions.

March OPEX Straddle: 232.8-point range suggests OPEX-to-OPEX movement between [6677, 7142].

March QOPEX Straddle: 368.55-point range projects [6466, 7203], based on December OPEX.

March EOM Straddle: 255.4-point straddle indicates a monthly range of [6623, 7101]. .

DEC2025 to DEC2026 OPEX straddle spans 945 points, outlining a range of [5889, 7779]."

DAILY VWAP BULLISH 6688

WEEKLY VWAP BEARISH 6777

MONTHLY VWAP BEARISH 6869

DAILY STRUCTURE – BALANCE - 6818/6627

WEEKLY STRUCTURE – OTFD - 6852

MONTHLY STRUCTURE - OTFD

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFD): This describ@es a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6785/75

GAMMA FLIP 6857.5

DAILY RANGE RES 6769 SUP 6707

2 SIGMA RES 6907 SUP 6641

VIX BULL BEAR ZONE 20

PUT/CALL RATIO 1.28 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Broad Rally’

S&P closed up +25bps at 6,716 with a Market on Close (MOC) imbalance of $1bn to buy. NDX rose +51bps to 24,780, R2K gained +67bps to 2,520, and the Dow edged up +10bps to 46,993. Trading volume across all U.S. equity exchanges totaled 16.9 billion shares, below the year-to-date daily average of 19.53 billion shares. The VIX dropped -4.76% to 22.4, WTI Crude surged +284bps to $96.18, the U.S. 10-Year Treasury yield fell -2bps to 4.20%, gold slipped -1bp to $5,005, the DXY declined -11bps to 99.60, and Bitcoin gained +30bps to $74,475.

It was a relatively quiet session, with trading volumes tracking -18% below the 20-day average. Equities posted modest gains, while crude oil climbed another +3%, nearing the $100 mark amid escalating tensions in the Middle East. Key developments included: 1) Iran targeting energy infrastructure such as the Shah gas field in the UAE and an Iraqi oil field; 2) Trump threatening expanded strikes on Kharg Island; 3) Israel reporting the death of Iran’s top security official, Larijani; 4) Trump delaying the China summit by five weeks; and 5) Trump asserting, “we do not need the help of anyone” regarding NATO. Brent/WTI currently reflects a $25/b risk premium.

Energy and macro-focused investors foresee significant upside for crude and refined products (diesel, jet fuel, gasoline) in the near term due to refinery disruptions, the ongoing Strait of Hormuz closure, and inventory drawdowns. Refining remains the most crowded long subsector, with jet fuel prices at record highs. Airlines, under pressure, saw a rally today following better-than-expected Q1 updates. Analysts anticipate upward revisions for Q1 and Q2 earnings. Large-cap refiners like VLO, MPC, and PSX are expected to prioritize buybacks.

In tech, a wave of new AI partnerships provided a boost to the sector and the broader market. Highlights include: 1) AMZN +1% after OpenAI signed an AWS deal aimed at securing government contracts, with Amazon’s CEO projecting AI to double AWS sales to $600B by 2036 (Reuters); 2) UBER +5% on NVIDIA’s announcement of launching robotaxis across 28 cities by 2028 (LYFT +3%); 3) CRWD +1.5% following a global partnership with Nebius; 4) INTC -3% as its Xeon 6 processors were announced as host CPUs in NVIDIA DGX Rubin NVL8 systems. Other notable moves: QCOM +2% after approving a $20B stock buyback and increasing its dividend.

Activity levels on the trading floor were rated a 4 out of 10. The floor ended +255bps to buy, compared to a 30-day average of +45bps. Asset managers and hedge funds were both net buyers, with ~$800m in net purchases. Long-only funds bought financials and macro products while selling healthcare and communication services. Hedge funds favored macro products but sold healthcare and energy. Short positions were broadly squeezed, rising +1.2%. ETF activity remained elevated at 35% of total trading volume. Top-of-book liquidity at $2.5mm returned to levels last seen on Liberation Day. Buyback activity is expected to slow as the blackout window begins this week (~March 18), with ~45% of S&P 500 companies entering blackout assuming a six-week lead time before earnings.

Looking ahead, tomorrow’s focus will be on macroeconomic data (U.S. PPI, Bank of Canada decision, U.S. factory/durable goods orders, and the FOMC decision) alongside earnings reports (pre-market: GIS, JBL, M, SAIL, Tencent, WSM; post-market: FIVE, MU) and analyst meetings (NVT).

In derivatives, the primary story was the significant volatility crush across major indices, particularly in the front end. April fixed strikes fell over a full volatility point in SPX/NDX/RUT. The VIX futures curve finally uninverted, but front-end skew saw renewed bids after a brief relaxation, with smaller moves further out on the curve. Notably, NDX is trading less than 3 vols above SPX in the front end, compared to ~5 vols earlier this month, reflecting a shift in demand for SPX/VIX hedges amid geopolitical uncertainty. On the flow side, investors are cautiously adding topside exposure after a prolonged drought in upside demand. The March FOMC decision is expected tomorrow, with the Fed with the Fed largely expected to hold rates steady - implied move for tomorrow: 0.87%.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!